Australia’s Big Four Banks – Commonwealth Bank of Australia (ASX: CBA), Westpac Banking Corporation (ASX: WBC), Australia and New Zealand Bank (ASX: ANZ), National Australia Bank (ASX: NAB) – have long been hailed as the envy of the world, generating the largest contribution to the GDP of the country in which they operate (2.9%), and ranked among the most profitable and safest in the world.

In FY 2023 collective profit from the Big Four Banks neared $32 billion dollars, a 12.4% increase over FY 2022.

As recently as March of 2023, an analysis of Tier One capital ratios from global investment bank Morgan Stanley found our Big Four “the best capitalised in the world.”

Australia’s Big Four

The Big Four have minimal competition for the Australian home mortgage loan market from regional and local small banks, but their main competition comes from each other. Collectively the Big Four Banks account for more than 90% of the market, as of mid-2022.

Top Australian Brokers

- Pepperstone - Trading education - Read our review

- IC Markets - Experienced and highly regulated - Read our review

- eToro - Social and copy trading platform - Read our review

The Big Four offer other banking services, from retail banking needs for savings, checking accounts, credit cards, and personal loans to wealth management services, primarily focusing on high-net-worth individuals and institutions. They also serve businesses with loans, cash management, payroll and other merchant services along with the more complex needs of large corporations such as capital financing.

All of the Big Four have insurance divisions, investment banking, and international banking.

The Big Four are essential to a healthy Australian Stock Exchange, with their market capitalisation collectively accounting for about 20% of the ASX 200 Index.

The higher interest rate environment did not prevent the Big Four’s record year in 2023, with reported loan growth defying higher rates and inflation concerns plaguing Aussie homebuyers. Some analysts now see the potential of a drop in the ability and willingness of Australian households to borrow and spend. Analysts are souring on the Big Four, but do they remain a good investment?

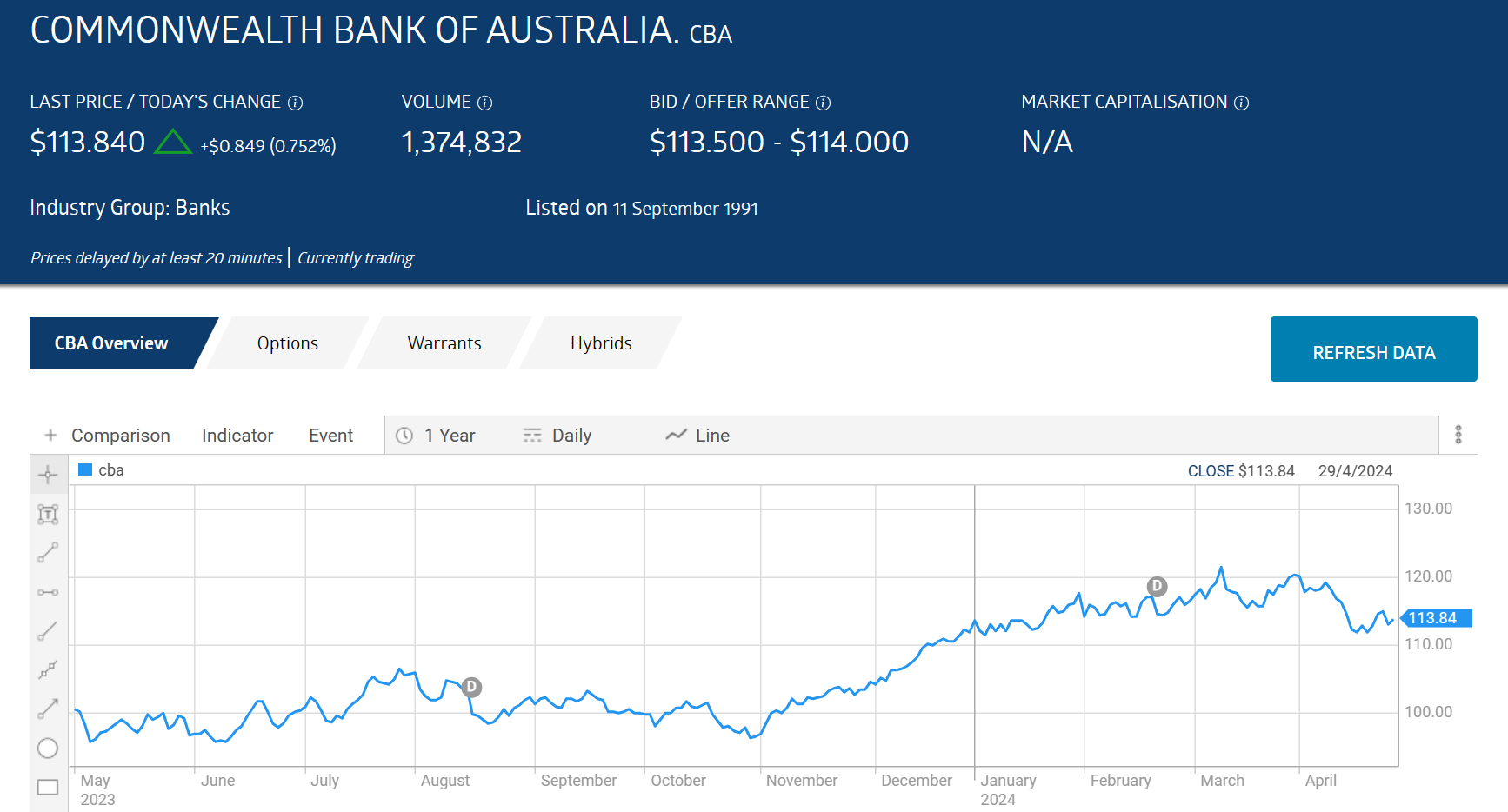

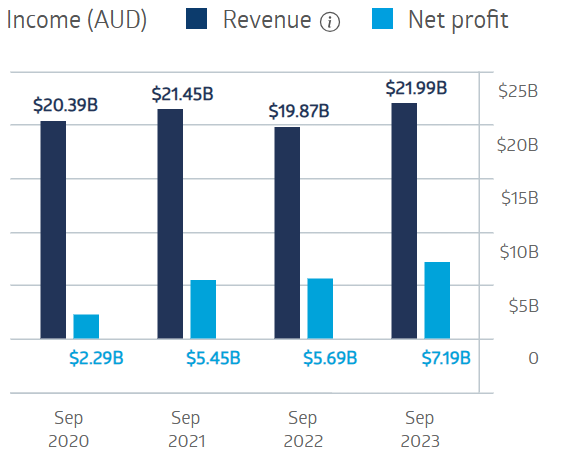

Commonwealth Bank of Australia (ASX: CBA)

Commonwealth Bank of Australia (ASX: CBA) is the largest of the three with the best share performance over five years of the Big Four – up 59.9%. Over ten years the share price is up 39.2%, justifying in the eyes of some investors the belief that share price appreciation is not a primary reason to invest in even the biggest of the Big Four Banks.

What draws investors is the dividend payments – and not just how much is paid out, but the reliability of the Big Four to continue paying even in down markets. While the Big Four have reduced dividends in market and economic downturns, they have not cut, even in the face of the COVID 19 pandemic where many ASX stocks eliminated dividends.

Commonwealth remains the biggest of the Big Four banks, but National Australia Bank now bests CBA in business banking, has risen to the second largest bank by market capitalisation, and has increased its share of the home mortgage loan business dominated by CBA.

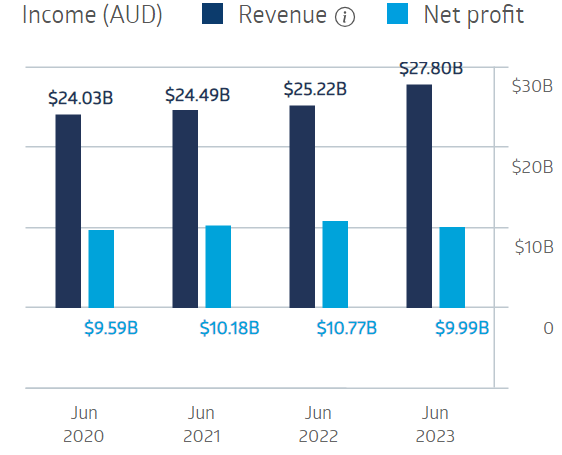

The bank’s financial performance over the last four fiscal years has been consistent and stable.

Commonwealth Bank of Australia Financial Performance

Source: ASX

Half Year 2024 results showed operating income increasing 0.2% while cash net profit after tax fell 3.1% and statutory net profit dropped 7.7%. Inflation drove operating expenses up 4.1% but Commonwealth Bank still raised its dividend payment by $0.05 per share. Management acknowledged “difficult conditions” going forward as consumers and businesses struggle in the high interest rate, high inflation environment.

In FY 2023 Commonwealth paid a dividend of $4.5 per share with a five-year average dividend yield of 4.03%. The bank cut its dividend payment in 2020 to $2.98 per share, down from $4.31 in FY 2019. Payments in 2021 and 2022 rose to $3.50 and 3.85.

On 23 April global investment bank Citi downgraded all four of the big banks. The concern is the prospect of the downside risk stemming from higher interest rates remaining in place.

Commonwealth is bearing the brunt of analyst angst, with the Wall Street Journal recommending investors SELL CBA stock. Of the seventeen analysts reporting, ten have SELL ratings, six have underweight, and one has a HOLD rating.

Marketscreener.com also has an analyst consensus rating of SELL, with nine of the fifteen analysts reporting at SELL and six at UNDERPERFORM.

Investors appear unconcerned as the CBA share price is up 14.7% year over year.

Source: ASX

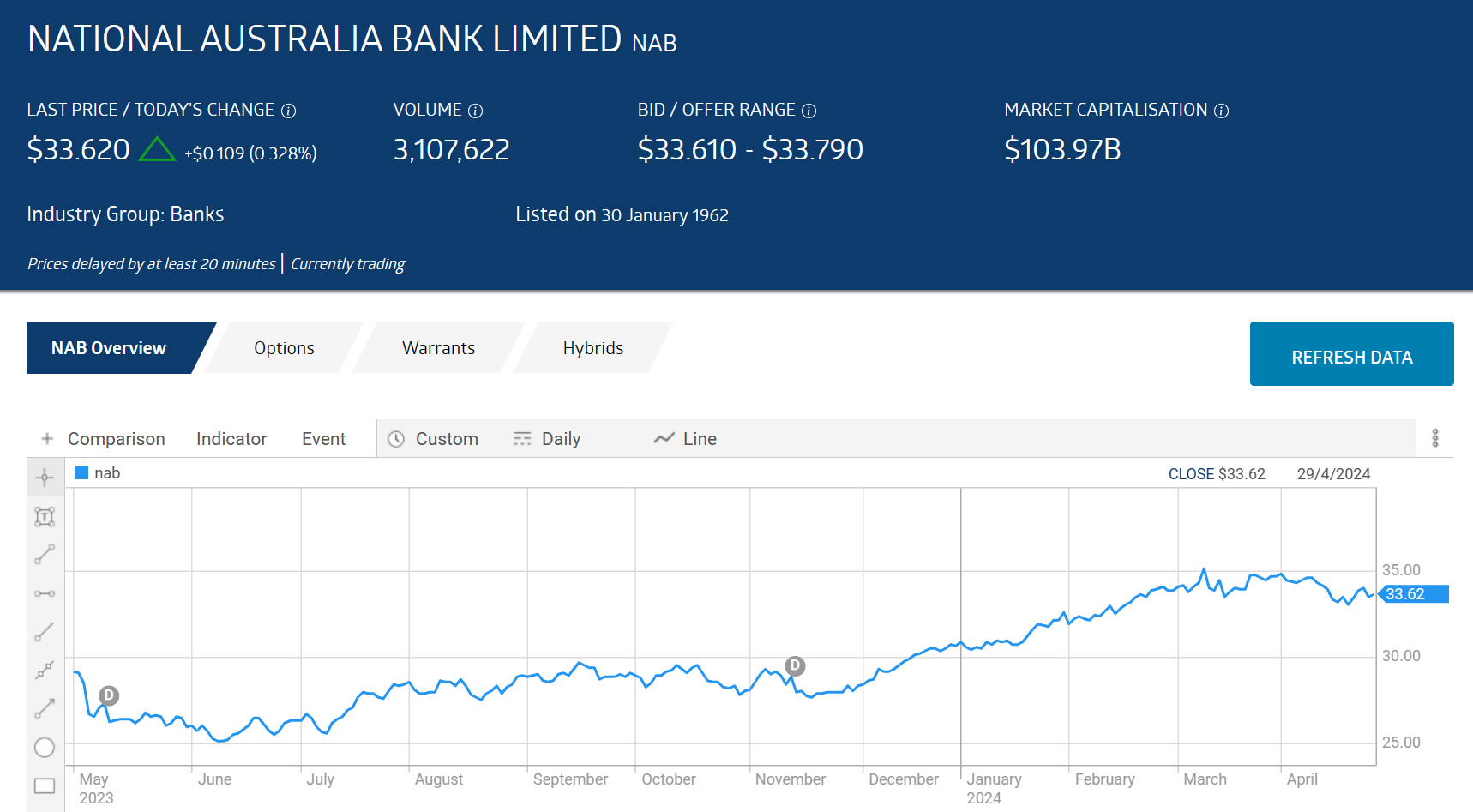

National Australia Bank (ASX: NAB)

National Australia Bank (ASX: NAB) is the second largest of the Big Four banks by market capitalisation. Although the differences among the Big Four might be considered minor, NAB is acknowledged as leading in business loans.

That edge was enough for global investment bank Goldman Sachs to buck the trend of negative analyst recommendations with a BUY on NAB shares and a price target of $33.89.

Year over year the share price is up 16.4%, as of 29 April of 2004. Over five years the share price is up 33%.

Source: ASX

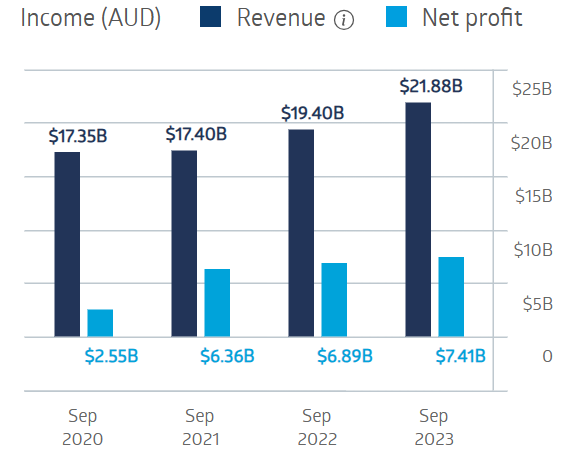

In the first year of the COVID pandemic NAB cut its dividend from $1.66 per share in FY 2019 to $.60 per share in FY 2020 before raising the dividends in FY 2021 to $1.27 followed by increases to $1.51 in FY 2022 and $1.67 per share in FY 2023. The five-year average dividend yield is 4.61%.

Like CBA, National Australia Banks’s financial performance has been consistent and stable.

National Australia Bank Financial Performance

Source: ASX

On 20 February NAB issued a trading update for the first quarter of FY 2024. Changes reflected a slower economic growth with a 16.9% decline in cash earnings compared to the first quarter of FY 2023. When compared to the second half of FY 2023 the decline was 3%. The bank did see a 2% increase in business loans and a 1% increase in home loans.

The Wall Street Journal has a HOLD recommendation on NAB shares, with two of the fifteen analysts reporting at BUY, one at OUTPERFORM, eight at HOLD, one at UNDERWE

IGHT, and three at SELL.

Marketscreener.com has an analyst consensus rating of UNDEFPERFORM on NAB, with three of the fourteen analysts reporting at OUTPERFORM, five at HOLD, two at UNDERPERFORM, and four at SELL.

Westpac Banking Corporation (ASX: WBC)

Westpac Banking Corporation (ASX: WBC) traces its history back to 1817 in New South Wales. The bank offers the same array of financial services to consumers, businesses, and institutions, claiming a “customer-centric” focus, as do all four of the banks.

Analyst concerns about the Big Four center on overvaluation exacerbated by rising share prices. However, on three key valuation ratios – price to earnings (P/E), price to book (P/B) and price to earnings growth (P/EG) the bank appears to be undervalued.

Westpac has a P/E of 13.20 against the index average of 19.46; a P/B of 1.14 against the benchmark index average of 2.24, and a P/EG of 0.51, well below the P/EG of 1.0 drawing the line between overvalued and undervalued stocks.

Year over year the share price is up 14.6% and down 0.62% over five years.

Source: ASX

Westpac cut its pre-COVID dividend payment from $1.74 per share to 0.31 in FY2020 before increasing to $1.18 in FY 2021, $1.25 in FY 2022 and $1.42 In FY 2023. The five-year average dividend yield is 4.26%. The bank has a solid track record of financial performance, with net profit increasing in each of the last four fiscal years.

Westpac Banking Corporation Financial Performance

Source: ASX

The Wall Street Journal has an UNDERWEIGHT rating on Westpac shares, with four of the sixteen analysts reporting at OVERWEIGHT, five at HOLD, one at UNDERWEIGHT, and six at SELL.

Marketscreener.com has an analyst consensus UNDERPERFORM rating on WBC shares, with one of the fourteen analysts reporting a BUY, two at OUTPEERFORM, five at HOLD, one at UNDERPERFORM, and five at SELL.

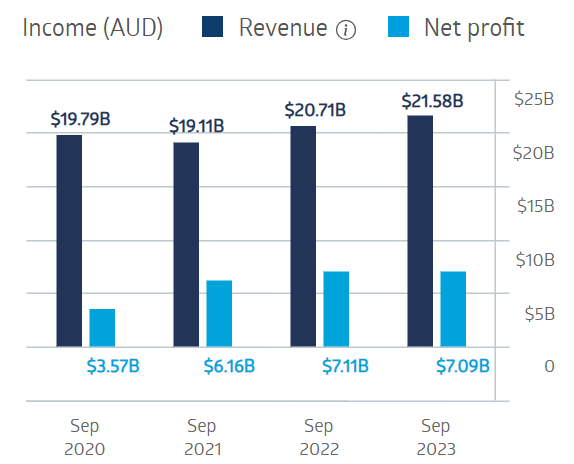

ANZ Group Holdings (ASX: ANZ)

ANZ Group Holdings (ASX: ANZ) has refocused onto its Australian and New Zealand operations away from its earlier intent to be more “Asia-centric.” That strategy has been replaced by an emphasis on the “higher returning” retail, business, and institutional customers here in Australia and in New Zealand.

On 20 February ANZ announced the Australian Competition Tribunal had approved ANZ’s acquisition of Suncorp Bank, with the intent of expanding ANZ’s retail and commercial operations while also improving services for Suncorp customers.

An analyst at UBS cited the acquisition as a “growth opportunity” for ANZ despite having a NEUTRAL rating on ANZ shares.

The bank’s Full Year 2023 results saw a revenue increase and a small decline in statutory net profit after tax. However, cash profit came in at a record $7.4 billion dollars. Dividend payments increased 20%.

ANZ Group Holdings Bank Financial Performance

Source: (ASX)

With a close of its business year in September, ANZ paid a dividend of $1.05 per share in FY 2020, rising to $1.42 in FY 2021 and $1.46 in FY 2022. FY 2023’s dividend was $1.88 with a dividend yield of 6.23% and a five-year average dividend yield of 4.96%.

The Wall Street Journal has a HOLD recommendation on ANZ shares with four of the fifteen analysts reporting at BUY, three at OVERWEIGHT, five at HOLD, and three at SELL.

Marketscreener.com also has a HOLD recommendation on ANZ, with 2 of the fourteen analysts reporting at BUY, three at OVERPERFORM, six at HOLD, and three at SELL.

ANZ’s valuation ratios make the stock a close second to WBC as a potentially undervalued stock, with a P/E of 12.35, a P/B of 1.21, and a P/EG of 0.53, all as of 29 April of 2024.

Year over year the share price is up 15% while over five years the share price is up 8.4%.

Source: ASX

Are Australia’s Big Four Banks a Good Investment?

Aussie investors looking for dividend income have some of the safest choices in the world in the Big Four Banks. The Big Four dominate the Australian banking market even with competition of regional and smaller local banks.

Commonwealth Bank is the largest but its three rivals offer similar services, making the choice of which bank to select for investing challenging. On valuation measures right now Westpac and ANX appear to be leading the pack.

The analyst community is bearish on the Big Four and will likely remain so until the interest rate picture in Australia becomes clearer and inflationary pressures cool.

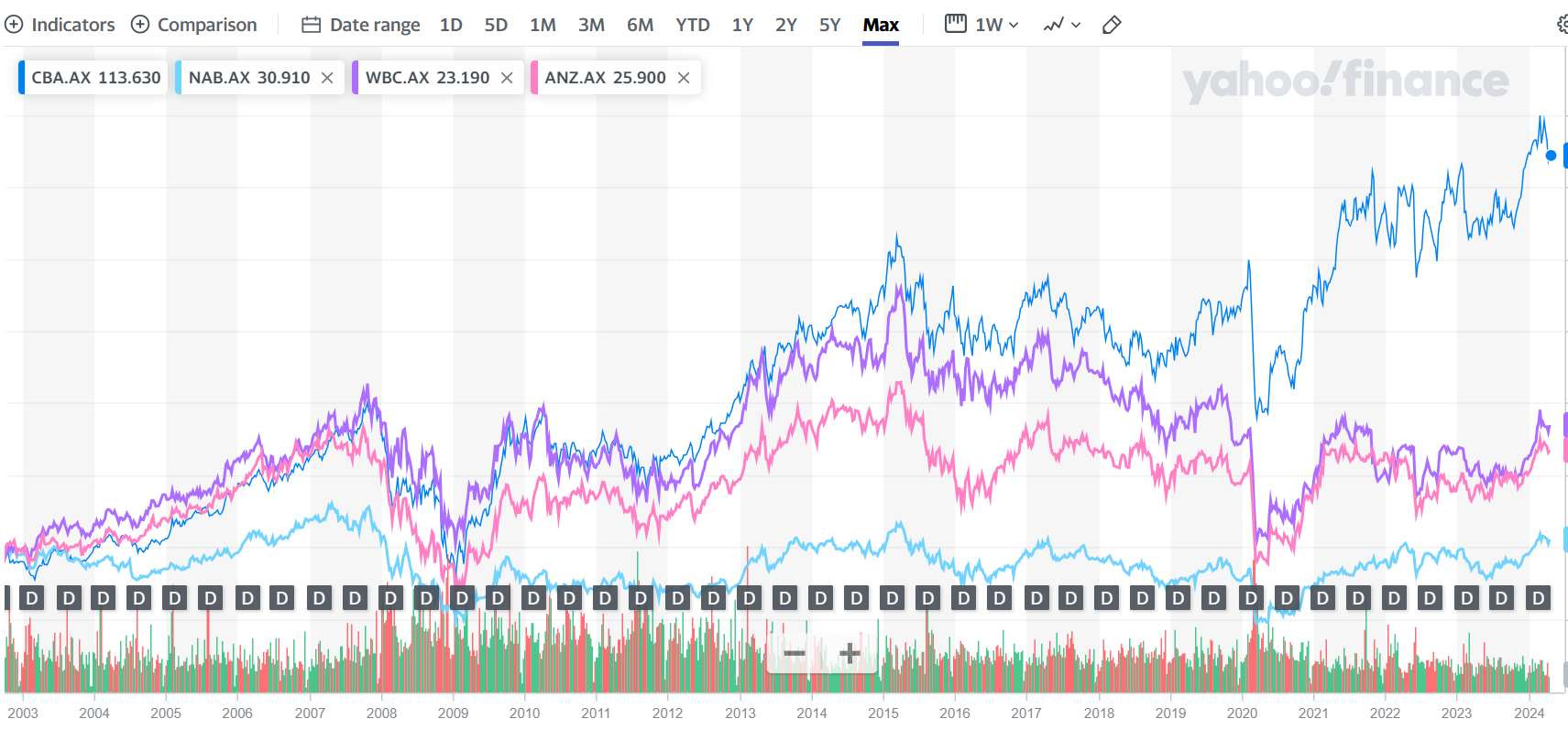

One thing is a near certainty – the Big Four are resilient. Indeed, resiliency may be as sound a reason for investing as are dividend payments.

The Big Four have survived the GFC, the Haynes Royal Commission, and the COVID 19 Pandemic. The following graph from yahoo finance Australia shows the price progression of each since listing as they weathered the GFC, the Haynes Commission, and now today’s challenging inflationary/high interest rate environment.

Source: Yahoo Finance Australia