Markets look set to close the year the way they spent most of it: volatile, fixated on central banks and worried about a recession.

Even though the data released this week more or less confirmed that inflation in the United States is past the peak, Fed Chair Jerome Powell and the rest of the Federal Open Market Committee stuck to the inflation-fighting script at their December meeting.

“We will stay the course,” Powell said, “until the job is done.”

At the European Central Bank (ECB) meeting on Thursday, President Christine Lagarde was even more forceful. Her comments strongly suggest that the ECB intends to raise rates aggressively through next spring despite the clear risks to economic growth in the region.

It seems like the central bank script hasn’t changed because there does still seem to be an imbalance in the labor market, and average hourly earnings are rising at a pace that isn’t consistent with 2% price inflation.

Top Australian Brokers

- Pepperstone - Trading education - Read our review

- IC Markets - Experienced and highly regulated - Read our review

- eToro - Social and copy trading platform - Read our review

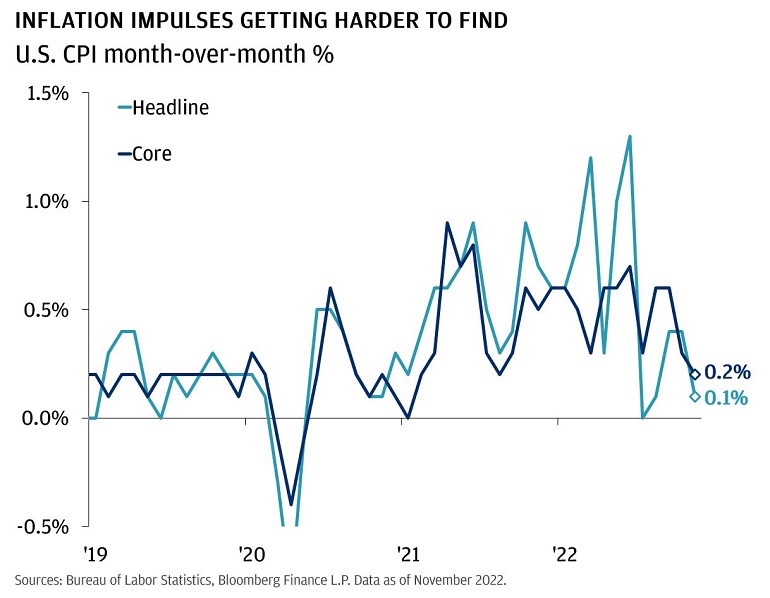

But the latest U.S. Consumer Price Index (CPI) data show a shrinking number of upside inflation drivers, especially when you consider that the official shelter price data are likely lagging actual conditions by a significant degree.

When inflation is high and sticky, strong talk from central bankers gets taken seriously by markets. But when interest rates are already slowing down growth, and actual inflation is running at a pace that is consistent with targets, markets can start to sniff out the end of the tightening cycle.

The bond market, for example, doesn’t seem to believe that the Federal Reserve will raise rates to over 5% like they say they will. Two-year bond yields are below the Federal Funds rate. Historically, that is a sign that investors think hiking cycles are over. The hawkish talk didn’t move longer-term rates either. 10-year bond yields are at their lowest level since September.

Even though stock markets had a shaky end to the week, they are still well above the lows from October.

In our outlook, we argued that the real economy will have to deal with the consequences of 2022’s rate hiking cycle, but markets are likely to find their footing. Despite the equity market volatility, the broad reaction to this week’s central bank meetings seem to support that view.

Spotlight: 2022 in Review

In our last note of the year, we wanted to take a look back on the year that was: challenges, tragedies, bright spots and all. So long 2022, we will see you in 2023!

All market and economic data as of December 16, 2022 and sourced from Bloomberg and FactSet unless otherwise stated.

The Standard and Poor’s 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Bloomberg Eco Surprise Index shows the degree to which economic analysts under- or over-estimate the trends in the business cycle. The surprise element is defined as the percentage difference between analyst forecasts and the published value of economic data releases.

Investing in fixed income products is subject to certain risks, including interest rate, credit, inflation, call, prepayment and reinvestment risk. Any fixed income security sold or redeemed prior to maturity may be subject to substantial gain or loss.

The price of equity securities may rise or fall due to the changes in the broad market or changes in a company’s financial condition, sometimes rapidly or unpredictably. Equity securities are subject to ‘stock market risk’ meaning that stock prices in general may decline over short or extended periods of time

We believe the information contained in this material to be reliable but do not warrant its accuracy or completeness. Opinions, estimates, and investment strategies and views expressed in this document constitute our judgment based on current market conditions and are subject to change without notice.

RISK CONSIDERATIONS

- Past performance is not indicative of future results. You may not invest directly in an index.

- The prices and rates of return are indicative, as they may vary over time based on market conditions.

- Additional risk considerations exist for all strategies.

- The information provided herein is not intended as a recommendation of or an offer or solicitation to purchase or sell any investment product or service.

- Opinions expressed herein may differ from the opinions expressed by other areas of J.P. Morgan. This material should not be regarded as investment research or a J.P. Morgan investment research report.

IMPORTANT INFORMATION

All companies referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by J.P. Morgan in this context.

Bonds are subject to interest rate risk, credit and default risk of the issuer. Bond prices generally fall when interest rates rise. Investing in fixed income products is subject to certain risks, including interest rate, credit, inflation, call, prepayment and reinvestment risk. Any fixed income security sold or redeemed prior to maturity may be subject to substantial gain or loss.