The biggest question relating to the management of the economy right now has nothing to do with next week’s budget. It has everything to do with the Reserve Bank and the board meetings that will follow it.

The question facing the board – the biggest there is when it comes to how the next few years are going to play out – is whether to hike interest rates just because prices are climbing.

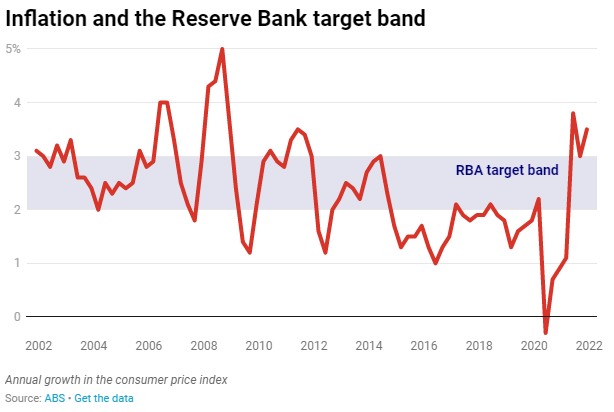

On the face of it, it seems like no question at all. It is widely believed that that’s what the Reserve Bank does, mechanically. When inflation climbs above 3% (it’s currently 3.5%) the board hikes interest rates to bring it back down to somewhere within the bank’s target band of 2-3%.

It’s what it did the last time inflation headed beyond its target zone in 2010.

Top Australian Brokers

- Pepperstone - Trading education - Read our review

- IC Markets - Experienced and highly regulated - Read our review

- eToro - Social and copy trading platform - Read our review

But the inflation we’ve got this time is different, and failing to recognise that misreads the bank’s rationale for pushing up rates, and what it is likely to do.

Inflation, but not as we’ve known it

The Reserve Bank does indeed target an inflation rate of 2-3%. The target is set down in a formal agreement with the treasurer, renewed each time a new treasurer or governor takes office.

Just about the only tool the bank has to achieve its inflation target is interest rates. If inflation is below the target, it can cut interest rates to make finance easier in the hope the extra money will encourage us to spend more and push up prices.

If inflation is above the target, it can push up rates so it becomes harder to borrow and interest payments become more onerous, taking money out of the economy and giving us less to push up prices with.

Here’s how the bank itself puts it:

If the economy is growing very strongly, demand is very buoyant and that’s pushing up prices, we might need to raise interest rates to slow the economy, to get things back onto an even keel.

Note the qualifier: “if demand is very buoyant and that’s pushing up prices”.

Buoyant demand (spending) is most certainly not the main thing pushing up prices now. The main things are beyond the Reserve Bank’s power to control.

Petrol prices have skyrocketed because of an invasion half a world away. It’s also the reason the global prices of wheat, barley and sunflower oil are climbing.

Food processors such as SPC say higher oil and food prices combined threaten to push up the price of a can of baked beans more than 20%.

The price of a set of tyres is set to climb from A$500 to $750 because tyres are made from oil.

Everything that is shipped and trucked using oil is set to cost more.

And trucks and cars themselves are climbing in price because of a global shortage of computer chips.

And it might get worse. Last week China locked down the high tech hub of Shenzhen, said to be the source of 90% of the world’s electronic goods, among them televisions, air conditioning units and smartphones. It reopened the city this week after testing its 17.5 million residents for COVID.

It’s easy to see why prices have shot up, and easy to see why they might not come down for a while. What is harder to see is how pushing up interest rates to crimp demand, to force Australians to spend less, would do anything to stop it.

What’s missing is inflation psychology

It’s a view Reserve Bank Governor Philip Lowe seems to endorse. He said this month that what he is on the lookout for is “inflation psychology” – the view that price rises will lead to wage rises, which will lead to price rises in an upward spiral.

It used to be how things worked. Australians who are old enough will remember when, if they saw something at a price they liked, they rushed out to buy it before it climbed in price. Australians born more recently have learnt not to bother.

The old psychology could come back, but wages growth – which would have to be high if that sort of thing was to happen – has remained historically low at 2.3%, little more than it was before COVID.

When surveyed, trade union officials expect little more (2.4%) in the year ahead.

It is true that these days most Australians aren’t in trade unions. So the Reserve Bank seeks out the views of ordinary households. On average, those surveyed expect wage growth in the year ahead of just 0.8%, which is next to nothing. The psychology hasn’t taken hold.

Until it does, it is best to think about most of what has happened as a series of isolated externally-driven price rises that have dented our standard of living.

Pushing up interest rates to dent living standards further won’t stop them.

The Reserve Bank is right to be on the lookout for internally-driven, self-sustaining inflation. We will know it when we see it – but we’re not seeing it yet.

Asked on ABC’s 7.30 this week whether there was a role for higher interest rates in an oil crisis, a former Reserve Bank board member, Warwick McKibbon, said

the worst thing a central bank can do in a supply shock or an oil crisis is to target inflation, because by targeting inflation you push downward pressure on the real economy

He went on to say that if the bank did it without success and then kept doing it, it would bring on a recession. I am sure the bank doesn’t want to do that.

Originally published by The Conversation

Author: Peter Martin Visiting Fellow, Crawford School of Public Policy, Australian National University