Right now, the market is trading based on one issue: inflation. This week was a bad one for inflation.

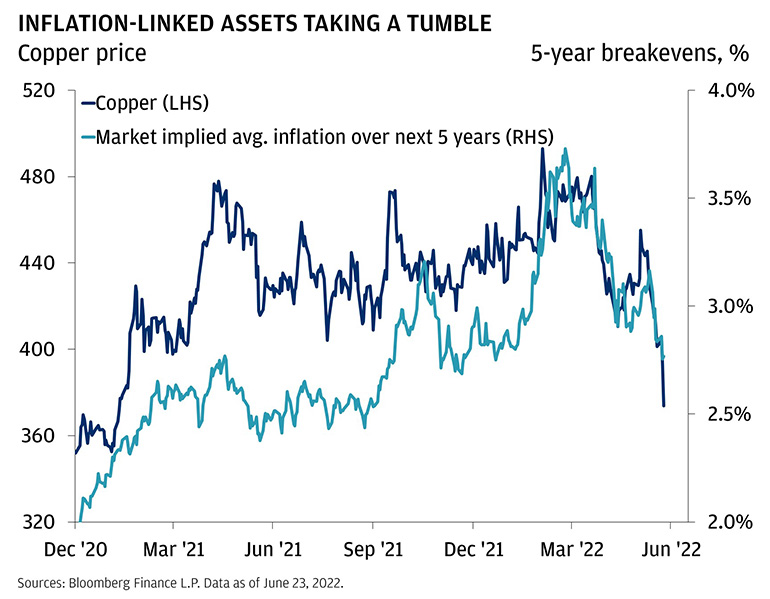

The selloff in oil and industrial commodities continued. Since last Friday, WTI crude has fallen over 11% and gasoline futures are down ~12% from recent highs. Copper is in its worst 10-day selloff since March 2020, when the whole world was heading into lockdown.

Bond yields followed suit. Ten-year yields are back below 3.1% after a spike up to 3.5% in the aftermath of the not-so-surprising policy rate hike of 75 basis points (bps) from the Federal Reserve. Two-year yields, which are more closely tied to policy rate expectations, plummeted back to 3% for the first time since May’s scorching CPI report. The market-implied expectations for average inflation over the next five years are at their lowest levels of the year, and have fallen 100 bps since their late March peak.

In equities, bond proxy and defensive sectors such as real estate, healthcare, utilities and consumer staples have led over the last five days, while the selloff in the energy sector continued (-13.5% this week, and now -24% down from the highs).

Notably, the speculative equities that have been most sensitive to rising bond yields have been hammering out a bottom. ARKK, the poster child of the current selloff, gained 19% and is now over 26% above the lows.

Top Australian Brokers

- Pepperstone - Trading education - Read our review

- IC Markets - Experienced and highly regulated - Read our review

- eToro - Social and copy trading platform - Read our review

At first, this all seemed like good news. The market mood has become very sour of late based on the premise that the Fed would have no choice but to cause a recession to tame inflation. Weakness in commodity prices gives policymakers more leeway to change course to avoid causing deeper economic damage.

The problem is that evidence is mounting that a growth slowdown is already well underway. The housing market is cooling very quickly due to higher mortgage rates, and the Purchasing Manager Indices (surveys of supply chain managers that have a reliable correlation with growth) came in well below expectations in June in both the United States and Europe. The latest data give credence to the idea that a self-reinforcing downturn may be already happening. From the Fed to The New York Times, to Cardi B, everyone sees it coming.

The recession everyone sees coming

On the first track of Jeezy’s seminal 2008 album The Recession, a news anchor says “no one’s whispering about the ‘R’ word anymore, now they just come right out and say it.”

Flash forward to 2022, and we are in the same position. In his testimony on Capitol Hill this week, Fed Chairman Jerome Powell admitted that it is going to be difficult to avoid a recession, given the current outlook for monetary policy. Google search trends for “recession” are even higher than they were during the COVID-19 lockdowns in April 2020, and a recent survey conducted by Yahoo and Maru Public Opinion found that over 80% of Americans believe we are either already in a recession or heading toward one. As we discussed last week, equity markets are already reflecting an elevated risk of recession, and both consumer and investor sentiments are historically negative.

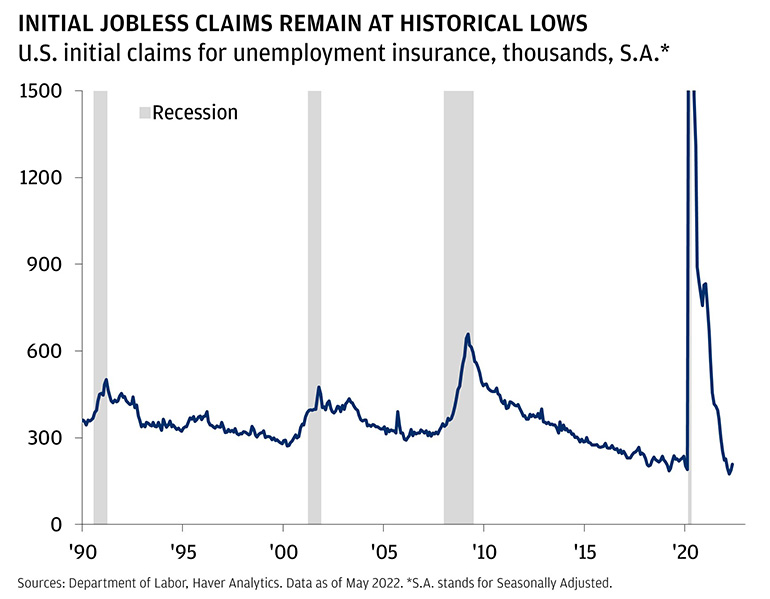

For the record, we do not believe the U.S. economy is currently in a recession. It all comes down to the labor market. Initial jobless claim have ticked higher, but are still at some of the lowest levels of the last 30 years. The economy has added over 500,000 jobs on average over the last six months, a rate that doubles the 2010s norm. But the point of the Fed’s current policy is to slow down that pace, and even its own forecasts are calling for job losses.

The answer to the question “are we heading for a recession?” matters to households, workers and business owners. Job losses, bankruptcies and business failures can be just as painful as inflation. For investors, the answer is still important, but the market, always looking ahead, has already started to reflect weakness. Based on the risk asset, we are somewhere between the “soft-ish” landing that Jerome Powell keeps talking about and full recession.

The path to those two most likely outcomes are more similar than they are different. As we move toward either a recession or soft-ish landing, growth will slow, inflation will fall, and the labor market will cool. What makes them different are the magnitude and duration of the slowdown. A peak unemployment rate of 4.1% (what the Fed could spin as a soft-ish landing) still necessitates almost one million job losses, but it is a much better outcome than a peak unemployment rate of, say, 6.5% (unquestionably a recession).

We still think a soft-ish landing is more likely than a recession, but the odds have narrowed. The most powerful evidence against a self-reinforcing downturn is the health of financial, corporate and household balance sheets. Weakening demand may not lead to the type of defaults and balance sheet stress that have exacerbated past downturns (see 2008–2009). Still, it will probably be a close call.

The similarities could give investors an advantage as they prepare portfolios. The same assets that should work heading into a recession are also the ones that will probably work heading into a soft-ish landing.

Investment takeaways

Given the likely path of slowing growth, falling inflation and a cooling labor market, we think investors should focus on three areas to help portfolios this summer. First, core fixed income still offers a valuable ballast to portfolios. Given the rally in fixed income markets this week, aggregate bond prices are in their best stretch of the year. If recession red flags continue to pop up, bond yields will likely fall further.

Second, quality equities should outperform as investors look to safe havens. We are looking for fortress balance sheets, high barriers to entry, reasonable valuations and steady cash flow streams. Finally, elevated volatility can provide investors with opportunities to enhance income or tailor more specific risk and return profiles using options. As always, tactical investors can look for dislocations in volatile markets.

Of course, all of this is dependent on each individual’s investment purpose, risk tolerance and stage of their respective investment process. For those building long-term multi-asset portfolios, both stocks and bonds are providing the most attractive entry point in years. For those who are uncomfortable with the amount of risk they are taking, the market is providing opportunities to reposition.

No matter the purpose, your J.P. Morgan team can help design the right portfolio for your financial goals.

All market and economic data as of June 16, 2022 and sourced from Bloomberg and FactSet unless otherwise stated.

We believe the information contained in this material to be reliable but do not warrant its accuracy or completeness. Opinions, estimates, and investment strategies and views expressed in this document constitute our judgment based on current market conditions and are subject to change without notice.

RISK CONSIDERATIONS

- Past performance is not indicative of future results. You may not invest directly in an index.

- The prices and rates of return are indicative, as they may vary over time based on market conditions.

- Additional risk considerations exist for all strategies.

- The information provided herein is not intended as a recommendation of or an offer or solicitation to purchase or sell any investment product or service.

- Opinions expressed herein may differ from the opinions expressed by other areas of J.P. Morgan. This material should not be regarded as investment research or a J.P. Morgan investment research report.

IMPORTANT INFORMATIONAll companies referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by J.P. Morgan in this context.

Bonds are subject to interest rate risk, credit and default risk of the issuer. Bond prices generally fall when interest rates rise. Investing in fixed income products is subject to certain risks, including interest rate, credit, inflation, call, prepayment and reinvestment risk. Any fixed income security sold or redeemed prior to maturity may be subject to substantial gain or loss.

All market and economic data as of May 2022 and sourced from Bloomberg and FactSet unless otherwise stated.

The information presented is not intended to be making value judgments on the preferred outcome of any government decision.