Inflation is a hot topic at the moment. We explain what it is and how it affects your spending, savings, loans and investments.

Inflation is a hot topic at the moment. But what exactly is it, and how does it affect you and your money?

Inflation is making news daily through wage inflation, energy inflation, food inflation, fuel inflation… and not just in Australia, but in many other countries too. In simple terms, inflation means that prices of things are steadily rising. Why does this matter? It means that unless our incomes rise in line with inflation, our money doesn’t go as far, and we might find it more difficult to buy the kinds of things that we’re used to having.

What is the definition of inflation?

Inflation is defined as an increase in prices of goods and services that are typically bought by households. Inflation is measured as the rate of change of those prices over time, hence the expression ‘inflation rate’.

Top Australian Brokers

- Pepperstone - Trading education - Read our review

- IC Markets - Experienced and highly regulated - Read our review

- eToro - Social and copy trading platform - Read our review

What is the inflation rate in Australia?

According to the most commonly used measure of inflation in Australia, the Consumer Price Index (CPI), inflation increased by 0.8% in the July to September 2021 quarter and rose 3% over the 12 months to September 2021.

Why does inflation happen?

There are two main causes of inflation:

- “Cost push inflation” is where the costs of producing goods or services goes up, and so price rises are passed onto customers. This could be because – as now – energy prices or labour costs are rising, for example.

- “Demand pull inflation” is when something is so popular that the supplier can’t meet the demand. Prices go up to reflect the lack of supply.

How is inflation measured?

The official Australian inflation measures come from the Australian Bureau of Statistics (ABS), which tracks prices of a ‘basket’ of commonly purchased goods and services. This is supposed to represent the spending of the average Australian household.

In deciding which goods and services to include in the CPI basket and what their weights should be, the ABS uses information about how much, and on what, people in Australia spend their income.

As people’s buying habits change, so do the goods and services that the ABS tracks. For example, in recent years, the ABS has added streaming services, ride sharing and smart phones to the CPI basket and removed items such as DVD hiring, cassette tapes and VCRs from the basket, to more adequately represent the average household expenditure. If households spend more of their income on one item, that item will have a larger weight n the CPI.

How is inflation controlled?

The Reserve Bank of Australia has a specific responsibility for low and stable inflation, full employment, and promoting the general welfare of the Australian people. The government has set a target of 2-3% for inflation, on average over time.

What does rising inflation mean for your spending?

Rising prices of goods and services will mean that unless your income rises too, you will find it more difficult to afford the things you normally buy. Sharp movements in the rate of inflation are not helpful either, because they make it difficult for people to plan their spending. For example, rising inflation can trigger “buy now while stocks last” behaviour.

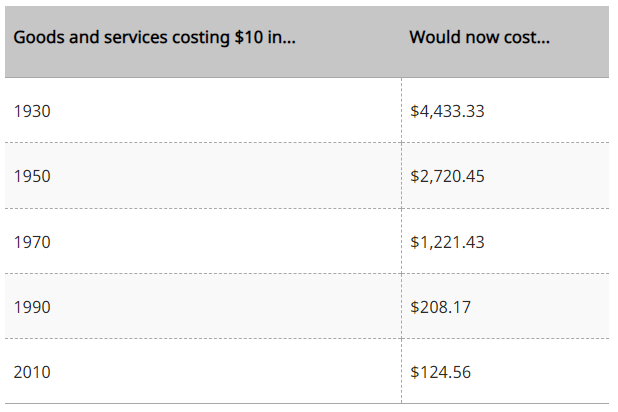

The following table shows how much you would need to spend today to equal $10 spent in each of the following years:

ABS CPI as at 30 September 2021.

What does high inflation mean for your savings?

If your savings don’t grow at a rate at least equal to inflation your wealth is shrinking. For example, inflation is now running at 3%, but cash in a current account is likely to earn less than 0.10% interest. Its value is being quietly eroded with every day that passes.

What does rising inflation mean for your loans?

The Reserve Bank tends to use interest rates as its primary tool to control inflation. As inflation rises, the Reserve Bank tends to be more willing to raise interest rates – meaning mortgages, loans and credit cards can become more expensive.

What does high inflation mean for your investments?

When inflation is rising, or already high, holding assets such as shares, property and bonds (or even foreign currency) can be more attractive than keeping your cash in a bank account (because, as inflation rises, the value of cash tends to fall relative to other types of assets) – but shifts in inflation and interest rate expectations can also spook investors, creating volatility and unpredictability in asset prices.

Originally published by Schroders