Even though factors such as supply chain issues have caused a slowdown, we still see room to grow in this expansion.

I’m an optimist, so I like to get the bad news out of the way first. Global stocks just had their worst month in a year. Companies such as Sherwin-Williams, Micron and Bed Bath & Beyond released weak guidance that blamed supply chain issues and building margin pressures. Analysts have a sinking feeling that those pre-announcements are just the prelude to what could be a disappointing third-quarter earnings season. Those supply chain issues and shortages, by the way, show little signs of improving. Vietnamese factories are shuttered due to COVID-19 outbreaks, natural gas prices are surging, British gas stations are out of, erm, petrol, and over 70 ships are waiting to offload their cargo at the Port of L.A./Long Beach.

In the background, economic data releases have been disappointing expectations, and consensus estimates for third-quarter GDP growth have fallen by two full percentage points from peak. Meanwhile, lawmakers on Capitol Hill are haggling over not only a physical infrastructure bill, but also a human infrastructure bill, and how to (or whether to) raise the debt ceiling. Even though we’ve avoided a government shutdown (thanks to yesterday’s last minute deal), the path forward for the three other items is far from clear.

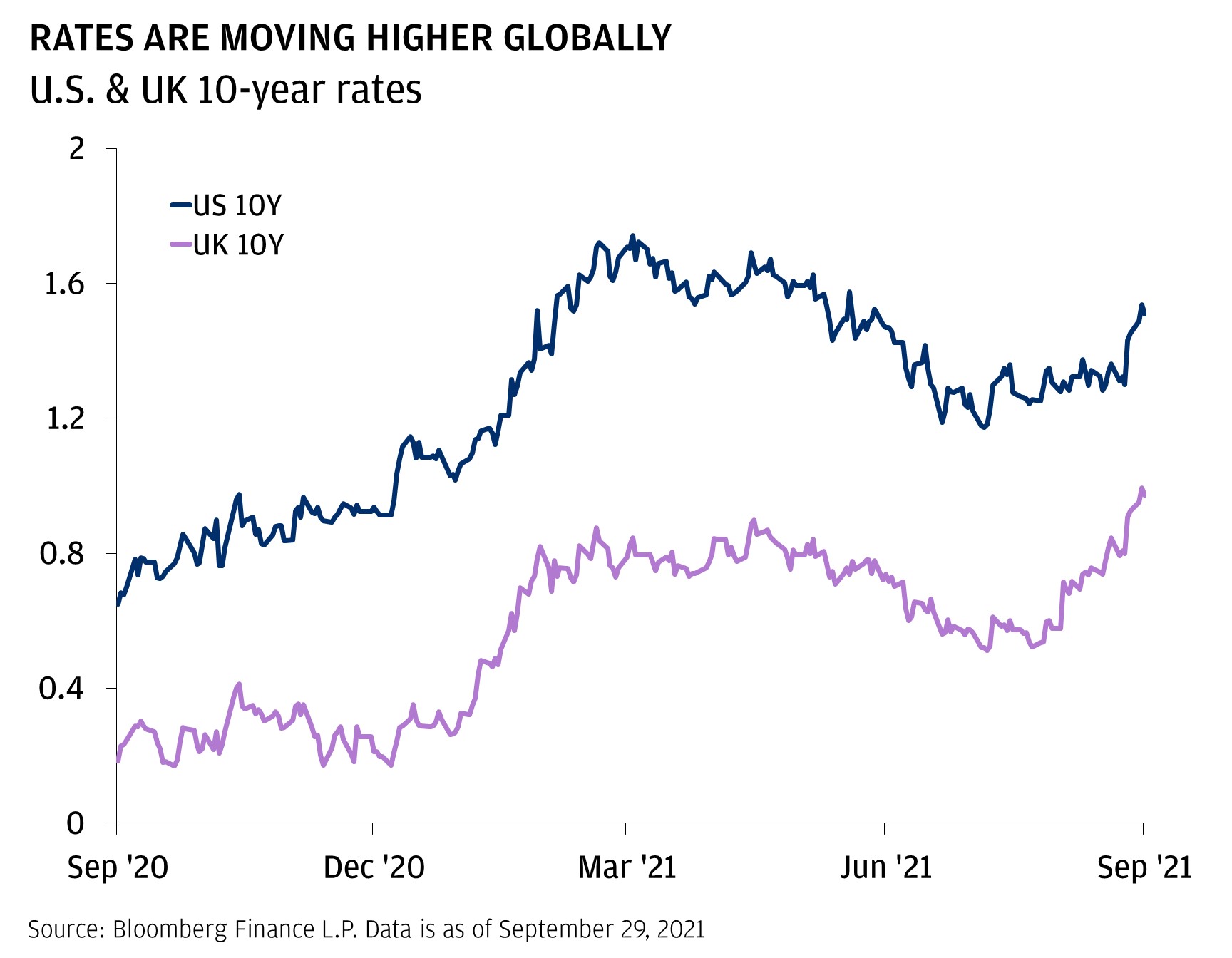

As if that wasn’t enough for investors to consider, interest rates around the world surged. In the United Kingdom, 10-year Gilt yields are above 1% for the first time since the spring of 2019. In Canada, yields are almost 40 basis points (bps) higher than they were at the beginning of August. In the United States, 10-year Treasury yields are up 25 bps over the last seven trading days, and 2-year yields are the highest they have been since the Federal Reserve cut policy rates to zero at the height of the COVID-19 crisis. Interest rates are like the foundation of a house. When they are unstable, problems start to show up elsewhere.

Top Australian Brokers

- Pepperstone - Trading education - Read our review

- IC Markets - Experienced and highly regulated - Read our review

- eToro - Social and copy trading platform - Read our review

Given that, it may not surprise you that the S&P 500 sold off sharply, and closed below its 100-day moving average for the first time since October 2020. As you would expect, the parts of the market that are more sensitive to rising interest rates, such as technology stocks (-6.5% from highs), utilities (-8%) and gold (-8%), are suffering.

For technology stocks, higher interest rates decrease the value of those further out cash flows investors have been expecting. Areas such as gold and utilities compete with bonds for capital seeking a “safe” haven. Higher rates mean that bonds look incrementally more attractive. But those moves are more or less mechanical. The spookier question that investors are asking is if this spike in bond yields, which raises borrowing costs for businesses and consumers, and therefore works to slow down economic growth, is coming at exactly the wrong time.

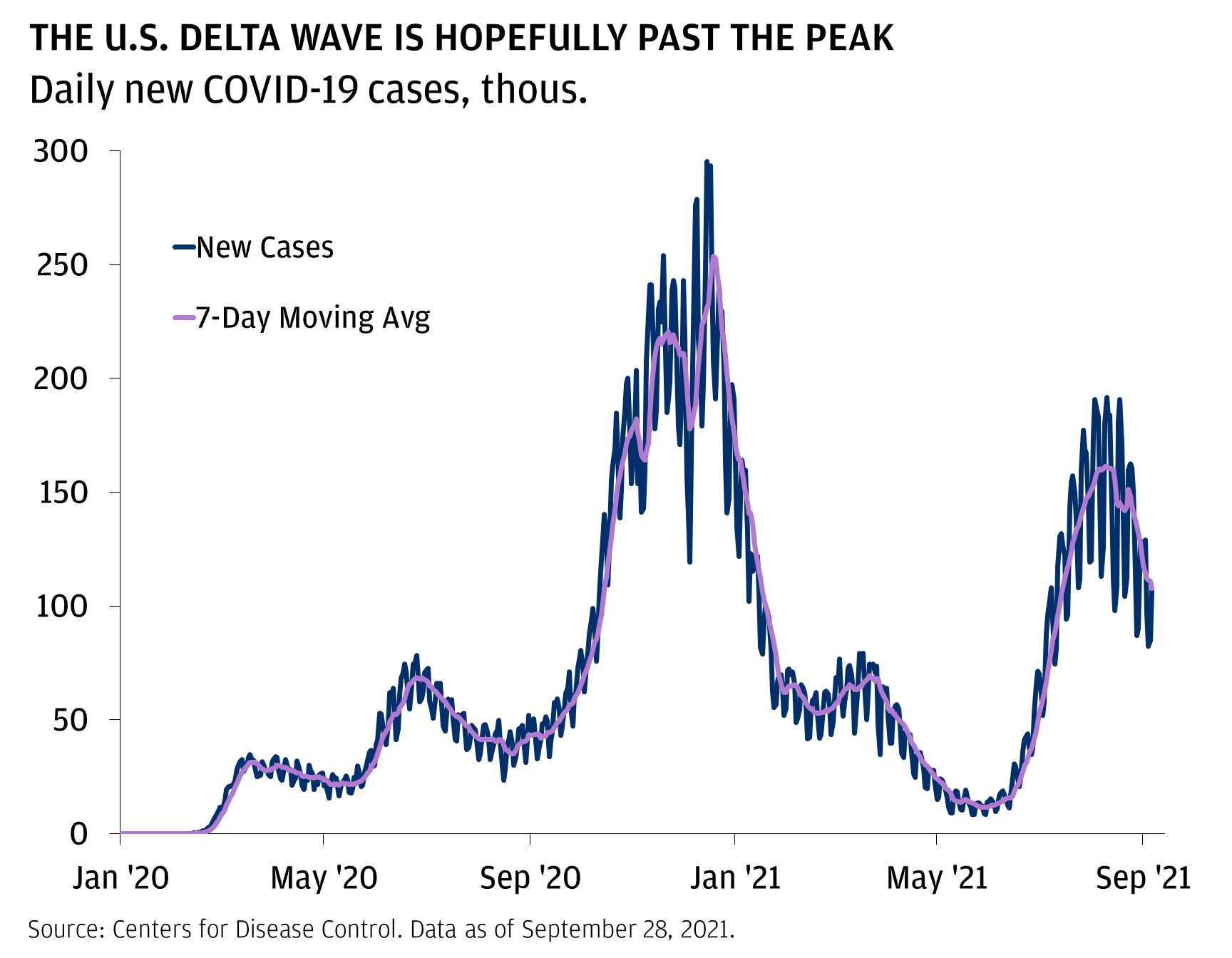

OK, that’s enough of the bad news. Here is the good news. Shifts toward tighter monetary policy from places such as the Fed and Bank of England could be jolting rates, but the more important driver may be that bond investors are expecting an improving macroeconomic backdrop going forward. Markets move on expectations and relativity. The Delta-driven COVID wave has hampered restaurant spending, hit travel bookings, disrupted supply chains and exacerbated shortages. But now, COVID cases are around 30% below the Delta wave peaks, and still receding both in the United States and on a global basis.

Stock markets have noticed, too. Global airline stocks are up +10% since their late August lows, and the energy sector is somehow up over +9% this month even though the broader market is down over -5%. In fact, economic data may still be missing expectations, but to a lesser degree than they were at the beginning of September. This week, both capital goods orders and pending home sales data beat expectations. Less bad for markets is as good as good.

The bear case for now seems as clear as it has all year. Central banks are removing policy support just as supply chain chaos and inflation prove to be intransient and growth is decelerating in the United States and China. However, we don’t believe interest rates pose a threat to the expansion at this point (corporate and household borrowing costs are still below expected returns), the supply chain issues are in part driven by robust demand (a good problem), and we still expect earnings growth to drive equity markets higher over the next 12 months.

Markets just might have to muddle through a soft patch for a little while longer.

In the meantime, investors should focus on quality companies that can work in either rising or falling rate environments, and continue to rely on dynamic active management to navigate what could be a turbulent period for fixed income.

Originally published by JP Morgan Australia.

Author: JACOB MANOUKIAN, U.S. HEAD OF INVESTMENT STRATEGY

All market and economic data as of October 2021 and sourced from Bloomberg and FactSet unless otherwise stated.

We believe the information contained in this material to be reliable but do not warrant its accuracy or completeness. Opinions, estimates, and investment strategies and views expressed in this document constitute our judgment based on current market conditions and are subject to change without notice.

RISK CONSIDERATIONS

Past performance is not indicative of future results. You may not invest directly in an index.

The prices and rates of return are indicative, as they may vary over time based on market conditions.

Additional risk considerations exist for all strategies.

The information provided herein is not intended as a recommendation of or an offer or solicitation to purchase or sell any investment product or service.

Opinions expressed herein may differ from the opinions expressed by other areas of J.P. Morgan. This material should not be regarded as investment research or a J.P. Morgan investment research report.

IMPORTANT INFORMATION

All companies referenced are shown for illustrative purposes only, and are not intended as a recommendation or endorsement by J.P. Morgan in this context.

All market and economic data as of October 2021 and sourced from Bloomberg and FactSet unless otherwise stated.

The information presented is not intended to be making value judgments on the preferred outcome of any government decision.