Angus Geddes, Fat Prophets

BUY RECOMMENDATIONS

Praemium (PPS)

This financial services platform provider recently revealed record inflows of $1.1 billion for the December 2020 quarter, up 128 per cent on the prior corresponding period. Global funds under administration increased by 10 per cent to $34.3 billion. In my view, the acquisition of Powerwrap will transform the company, with scale benefits already starting to emerge. Praemium’s UK business is also tracking nicely. PPS also offers operational momentum.

The Reject Shop (TRS)

This discount store chain is a turnaround play, with new management at the helm. The discount variety sector appears under-represented in Australia, and competition is arguably weaker compared to other developed countries. TRS offers potential long term growth, as the store network expands during the next few years. Any reduction in commercial rents would assist these endeavours.

HOLD RECOMMENDATIONS

BHP Group (BHP)

The company is leveraged to our bullish view on iron ore, which should drive cash flows and dividends higher. BHP is committed to shipping between 276 million tonnes and 286 million tonnes of iron ore from the Pilbara in the year to June 30. Other parts of BHP’s business appear to be tracking well.

Fortescue Metals Group (FMG)

The iron ore producer is enjoying strong momentum. Higher iron ore prices contributed to the company’s unaudited net profit after tax of $US940 million for the month of December. The company expects first half net profit after tax to range between $US4 billion and $US4.1 billion when results are released later this month.

Shareholders can expect an attractive dividend.

SELL RECOMMENDATIONS

Coca-Cola Amatil (CCL)

The beverage maker recently released a strong trading update, with soft drink, water and juice volumes returning to growth in Australia for the December quarter. Australian volumes were up 0.4 per cent on the prior corresponding period. CCL’s improving performance may prompt shareholders to seek a higher takeover bid than the $9 billion offered by Coca-Cola European Partners. In our view, there’s a risk the bid could fail at $12.75 a share.

Tuas (TUA)

Investors in TPG Telecom received shares in Tuas following last year’s merger with Vodafone Hutchison Australia. Through a subsidiary, Tuas owns and operates a 4G mobile network in Singapore, but was impacted after failing to obtain a 5G wholesale licence. TUA is cashed up and has strong asset backing. It may be worthwhile for shareholders to consider selling TUA, before buying TPG, which has strong domestic synergies ahead following last year’s merger.

Disclosure: Interests associated with Fat Prophets hold shares in PPS, TRS, BHP, FMG and TPG.

Tony Locantro, Alto Capital

BUY RECOMMENDATIONS

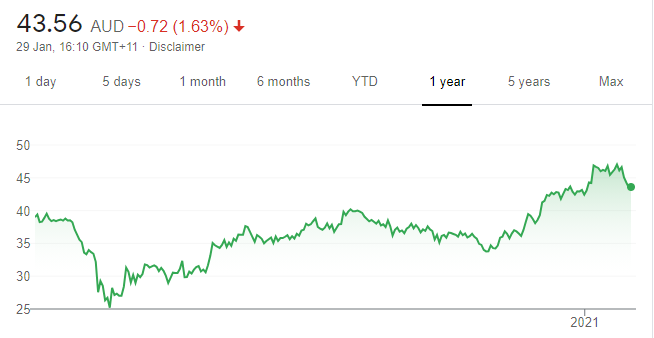

Aurumin (AUN)

Top Australian Brokers

- Pepperstone - multi-asset Australian broker - Read our review

- eToro - market-leading social trading platform - Read our review

- IC Markets - experienced and highly regulated - Read our review

We believe this recent listing offers an attractive growth opportunity in the junior gold sector. Key gold projects, Mount Dimer and Mount Palmer, offer significant exploration potential given previous high grade resources. Management has extensive experience in exploration, development and corporate finance. The shares have fallen from 35 cents on December 11 to close at 25 cents on January 28.

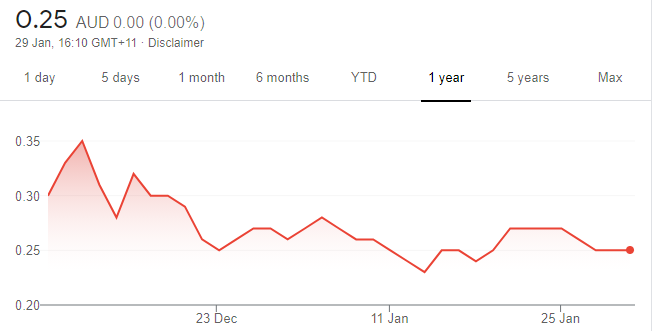

Chimeric Therapeutics (CHM)

This drug development company raised $35 million at 20 cents a share in its initial public offering. The company is focusing on developing an oncology pipeline of novel cell therapies to treat tumors. A phase 1 trial is underway at the City of Hope Cancer Centre in Los Angeles. The first patient was dosed in late 2020. Potential exists, but so do the risks. In our view, CHM is a highly speculative play for those with an appetite for risk. The shares closed at 33.5 cents on January 28.

HOLD RECOMMENDATIONS

Nyrada Inc. (NYR)

A company study revealed encouraging results in mice, with a 57 per cent reduction in total cholesterol. Additional laboratory test results revealed lower levels of the bad cholesterol. The next study will combine the company’s lead product candidate with a statin, and results are expected by the middle of this year. NYR is also developing treatments for traumatic brain injury. We anticipate further news relating to lead candidates as they move through pre-clinical stages.

Godolphin Resources (GRL)

The company recently announced a revised mineral resource estimate for the Lewis Ponds deposit in New South Wales. The resource calculation has revealed 384,000 ounces of gold, 15.3 million ounces of silver, 158,000 tonnes of zinc, 93,000 tonnes of lead and 10,000 tonnes of copper. The Copper Hill East target is being tested with deeper drilling. In our view, GRL is a high risk/high reward play.

SELL RECOMMENDATIONS

JB Hi-Fi (JBH)

The consumer electronics giant posted an impressive unaudited half year net profit after tax of $317.7 million, an increase of 86.2 per cent on the prior corresponding period. Online sales were up 161.7 per cent to $678.8 million. There’s a risk future growth may not meet expectations as Federal Government stimulus is scaled down. Share price strength represents a profit taking opportunity.

Woolworths Group (WOW)

The supermarket giant has been a strong performer. The share price has risen from $37.65 on December 1 to close at $41 on January 28. WOW is regarded as a defensive stock, but, in our view, it’s currently priced as a growth stock, as it was recently trading on a price/earning multiple of about 44 times. We believe risk remains to the downside, so investors can consider taking profits.

Tony Paterno, Ord Minnett

BUY RECOMMENDATIONS

Sezzle Inc. (SZL)

This buy now, pay later platform provider delivered a strong fourth quarter performance. Underlying merchant sales rose 205 per cent on the prior corresponding period to $US320.8 million. Active merchants substantially grew to 26,690. Repeat customer usage has remained strong. In our view, the growth outlook is bright. The stock is trading at a substantial discount to market darling Afterpay on an enterprise value to sales basis.

Nine Entertainment Co. Holdings (NEC)

A recent update from the media giant revealed improving trading conditions. The company now expects metro free-to-air advertising revenue growth of almost 20 per cent for the December quarter. It had been expecting 15 per cent. The group’s metro TV advertising revenues for the December half are forecast to rise by about 1 per cent on the same period last year. First half EBITDA before specific items is expected to be up by more than 40 per cent on the prior corresponding period. Previous guidance was 30 per cent.

HOLD RECOMMENDATIONS

Home Consortium (HMC)

The company plans to further build its funds management platform by launching a health, wellness and government-focused fund in early 2021. The company is working towards a target of more than $5 billion in assets under management. HMC has a strong growth trajectory and we retain our hold recommendation.

Downer EDI (DOW)

This integrated services provider has agreed to sell its open cut mining west business to Perth-based mining contractor MACA. The sale is part of Downer’s urban services strategy to exit its capital intensive mining business. According to our calculations, the company appears to be selling its mining services units at book value. In our view, the sale is a positive step in executing the Downer strategy, although selling at book value is modestly value dilutive, based on our modelling.

SELL RECOMMENDATIONS

Worley (WOR)

The company sees substantial growth opportunities in environmental, social and corporate governance related projects. While this engineering services provider is well placed to capitalise on growth, these projects represent a small portion of current revenue. The near term outlook remains challenging with projects deferred, resulting in a reduced headcount – a key metric, in our view. The stock looks expensive to us and consensus forecasts appear optimistic.

ALE Property Group (LEP)

A management priority is to continue paying a predictable distribution, increasing by at least the consumer price index each year. It will retain an investment grade credit rating. Gearing is likely to rise, as LEP continues to pay out more than it’s earning. Our estimates assume a payout ratio of between 125 per cent and 130 per cent of operating earnings for fiscal year 2022 and beyond. Better opportunities exist elsewhere at this point, in our view.

The above recommendations are general advice and don’t take into account any individual’s objectives, financial situation or needs. Investors are advised to seek their own professional advice before investing. Please note that TheBull.com.au simply publishes broker recommendations on this page. The publication of these recommendations does not in any way constitute a recommendation on the part of TheBull.com.au. You should seek professional advice before making any investment decisions.