Michael Gable, Fairmont Equities

BUY RECOMMENDATIONS

Wesfarmers (WES)

This industrial conglomerate has formed a cup and handle on the technical chart. This is a response to the share price dipping from its February peak and re-testing it in April. Then the share price congested below its peak for longer than anticipated. An eventual break above $56 a share triggered a buy signal. The share price was trading at $57.49 on June 24. The stock offers a bright outlook, in our view.

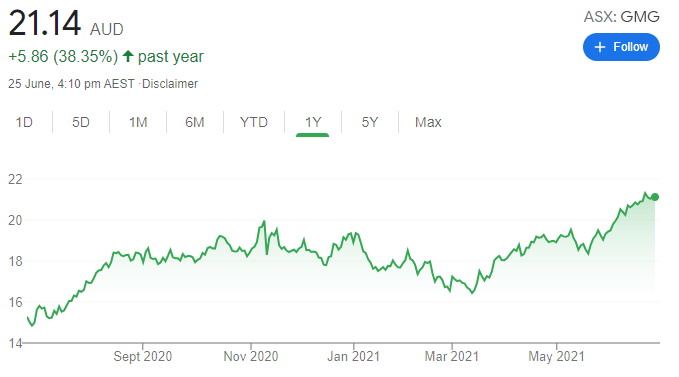

Goodman Group (GMG)

We consider GMG a growth and defensive stock due to its exposure to industrial property across the globe. From a charting perspective, the share price finally breached the crucial resistance level of $20 a few weeks ago. Healthy trading volumes show buyers returning to the stock. The stock was trading at $20.92 on June 24. We expect it to move higher from here.

HOLD RECOMMENDATIONS

CSL (CSL)

The share price bounced strongly in March, and has continued to trend higher. The shares have risen from $246 on March 8 to recently trade above $300. We consider CSL a growth stock, so it should benefit from any easing in long term bond yields. Also, this blood products group has a strong track record of delivering good results. The shares were trading at $290.11 on June 24.

Aristocrat Leisure (ALL)

Since upgrading earnings guidance several weeks ago, the shares have enjoyed good buying support. This gaming company has been making all time highs recently, and the chart still looks bullish. We believe positive share price momentum can continue on the back of strong earnings growth.

SELL RECOMMENDATIONS

Perpetual (PPT)

The share price of this diversified financial services business has risen by more than $10 since early November last year. It was undervalued when it rose, so it attracted investors in a buoyant market. In our view, investors may want to consider taking a profit because we see resistance ahead on the technical chart. The shares were trading at $38.94 on June 24.

Nufarm (NUF)

This crop protection company was priced at $5.60 on April 23. The share price has been drifting to trade at $4.67 on June 24. The technical chart is telling us that selling pressure remains. The share price is finding it difficult to rally at this point. It may one day, but not in the short term, in our opinion.

James Massey, Argonaut

BUY RECOMMENDATIONS

Nutritional Growth Solutions (NGS)

NGS develops, produces and sells clinically tested nutritional supplement formula for children. It recently signed a memorandum of understanding to produce its Healthy Height product in New Zealand for the Chinese and Asia Pacific markets. The shares have risen from 17 cents on June 22 to close at 18.5 cents on June 24. Good management and the company’s growth strategy paint a bright outlook, in our opinion.

Genesis Minerals (GMD)

Top Australian Brokers

- Pepperstone - multi-asset Australian broker - Read our review

- eToro - market-leading social trading platform - Read our review

- IC Markets - experienced and highly regulated - Read our review

Genesis Minerals is a gold exploration and mine development company. The company’s flagship Ulysses project is located north of Kalgoorlie. Recent results from the Admiral Deeps and Puzzle North zones demonstrate significant exploration upside at Ulysses. We see Ulysses as a project that supports a stand-alone mining operation. We anticipate future exploration success.

HOLD RECOMMENDATIONS

Medallion Metals (MM8)

This minerals explorer owns the Ravensthorpe gold project and the Jerdacuttup base metals project in Western Australia. Results support historical drilling at the Gem Restored prospect and a potential new mineralised lode was identified. These results appear to be a positive first step.

Global Lithium Resources (GL1)

GL1 recently acquired more than 120 square kilometres of prospective lithium tenure in Western Australia’s Pilbara region. It almost doubles the size of its project landholding. The company has completed an RC (reverse circulation) drilling program, comprising 36 holes, at its Marble Bar Lithium Project. Hold for assay results anticipated later this year.

SELL RECOMMENDATIONS

Emerald Resources NL (EMR)

This explorer and developer recently announced a maiden gold pour at its Okvau mine in Cambodia. Management has a good track record. The company’s market capitalisation was about $463.85 million on June 24. We’re concerned about jurisdiction risk. The shares have drifted from $1.105 on June 1 to close at 90 cents on June 24.

Elixir Energy (EXR)

This gas explorer is focused on Mongolia. The company’s market capitalisation was about $240.57 million on June 24. We’re concerned about jurisdiction and execution risks when it comes to development. The share price has fallen from 45.5 cents on April 15 to close at 26 cents on June 24.

Tony Paterno, Ord Minnett

BUY RECOMMENDATIONS

Rio Tinto (RIO)

The feasibility study on its Jadar lithium project in Serbia is due to be completed later this year. We believe management is likely to approve the project due to the positive environmental, social and governance credentials. The outlook for strong lithium demand would also be appealing. Jadar could reach full production in 2028, supplying about 3.5 per cent of global lithium. According to our analysis, the Jadar project would contribute 1.5 per cent or $US400 million to Rio Tinto’s operating earnings.

Macquarie Group (MQG)

Macquarie Infrastructure Corporation announced the sale of Atlantic Aviation to KKR for $US4.475 billion in cash, along with assumed debt and re-organisation obligations. Macquarie Group, as external manager, will earn a $A290 million disposition payment. The transaction reflects a robust environment for infrastructure assets and, in our view, should support performance fees and investment income for Macquarie Group in fiscal year 2022.

HOLD RECOMMENDATIONS

The Reject Shop (TRS)

The retail chain’s initial turnaround has been underpinned by a stronger balance sheet and cost cutting. However, the turnaround has a long way to run. We expect sales revenue to decline 11 per cent in the second half of fiscal year 2021. It will take time to yield improving and more consistent results across the chain amid re-negotiating store leases.

Dexus (DXS)

The real estate group upgraded its fiscal year 2021 dividend guidance from flat to about 3 per cent growth on the prior year. Dexus also noted it achieved better-than-expected outcomes on leasing, rents, capital expenditure, incentives and rent relief. The downside is Rio Tinto departing its existing Brisbane headquarters soon for another address.

SELL RECOMMENDATIONS

Xero (XRO)

We have updated our financial model to reflect an increase in average revenue per user from the second half of fiscal year 2022. According to our analysis, Xero’s average revenue per user has been relatively stagnant in the past two years. Price increases had been delayed due to COVID-19. The share price of this accounting software company has enjoyed a strong run in the past 12 months. Investors may want to consider taking a profit.

Oz Minerals (OZL)

The copper price recently hit all-time highs. The Oz Minerals share price has doubled in the past 12 months. The share price was recently trading at a 20 per cent premium to our net present value. OZL has a strong growth pipeline, but compared to its peers, we believe the stock appears expensive. The share price was trading at $22.49 on June 24.

The above recommendations are general advice and don’t take into account any individual’s objectives, financial situation or needs. Investors are advised to seek their own professional advice before investing. Please note that TheBull.com.au simply publishes broker recommendations on this page. The publication of these recommendations does not in any way constitute a recommendation on the part of TheBull.com.au. You should seek professional advice before making any investment decisions.