John Athanasiou, Red Leaf Securities

BUY RECOMMENDATIONS

BlueBet Holdings (BBT)

This sports betting technology company had cash and cash equivalents of about $51 million at the end of the third quarter of fiscal year 2022. Also, BBT is expanding in the lucrative US market. It recently signed a 10-year market access agreement to operate in Indiana. Gambling stocks traditionally do well during challenging times, and we believe this will be the case with BBT.

Cleanaway Waste Management (CWY)

The waste management company has a dominant position in an industry with high barriers to entry. The bulk of the company’s revenues are generated from recurring multi-year contracts. In May, the company downgraded earnings due to floods and higher fuel and labour costs. Despite a lag in cost recoveries, CWY’s longer term outlook is bright.

HOLD RECOMMENDATIONS

New Hope Corporation (NHC)

The share price has risen from $3.21 on June 20 to trade at $4.35 on July 28. Rising coal prices have contributed to the share price rise. NHC is well managed. Investors should consider holding at these levels and monitor the momentum in coal prices before making a decision to adjust their level of shares.

Iluka Resources (ILU)

The mineral sands miner recently posted a strong production report. The company has committed to building a $1.2 billion rare earths refinery at Eneabba in Western Australia. In our view, investors should consider holding and monitor progress of the project via news flow.

SELL RECOMMENDATIONS

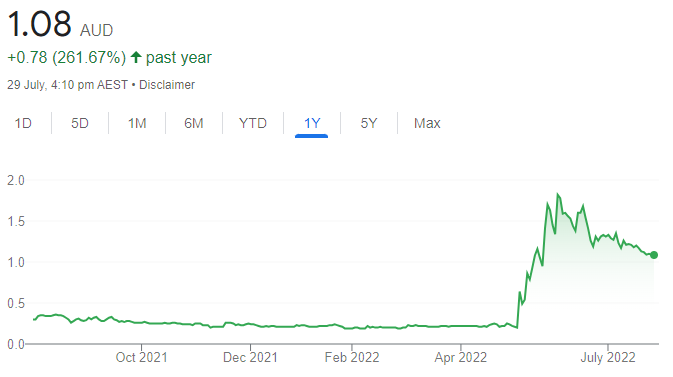

Galileo Mining (GAL)

The nickel explorer has been one of the best performing stocks on the ASX. In our view, the company has unveiled encouraging drilling results. It’s also raised about $20 million in capital. The shares have risen from 20 cents on May 6 to trade at $1.095 on July 28. Investors may want to consider cashing in some gains.

Woodside Energy Group (WDS)

The merge of BHP Group’s oil and gas portfolio with Woodside has created an energy powerhouse. Woodside is well managed. The share price has enjoyed a strong run since the start of 2022. We believe high energy prices are likely to fall, particularly if the supply crisis eases. Investors may want to consider locking in a profit.

Peter Moran, Wilsons

BUY RECOMMENDATIONS

Plenti Group (PLT)

The online lender has generated solid loan growth in recent years, driven by its personal and automotive lending divisions. Plenti’s level of new originations in the first quarter of fiscal year 2023 fell by 10 per cent on the prior quarter. However, this reflects its focus on increasing profitability at a time of rising interest rates. We retain an overweight rating.

Top Australian Brokers

- Pepperstone - multi-asset Australian broker - Read our review

- eToro - market-leading social trading platform - Read our review

- IC Markets - experienced and highly regulated - Read our review

Silk Laser Australia (SLA)

The share price of this laser clinic operator reflects a weak outlook, but we believe it’s been overdone. Although consumer spending is likely to fall in response to higher interest rates, we expect personal service providers, such as Silk, to benefit as consumers focus on what’s most important to them. We retain an overweight rating.

HOLD RECOMMENDATIONS

Breville Group (BRG)

This well managed kitchenware company has a solid track record of product development. However, the company is trading on a lofty premium compared to most of its international consumer product competitors. We hold a market weight rating, but expect the next 12 months to be more difficult as higher interest rates weigh on consumer spending.

Pacific Smiles Group (PSQ)

We have recently downgraded our recommendation for this owner of Australian dental clinics. We still expect the company to grow by continuing to add new centres. However, in our view, it’s taking longer than expected for new centres to become profitable, so we’ve moved to a market weight recommendation.

SELL RECOMMENDATIONS

Elders (ELD)

This provider of products and services to the agricultural sector has benefited from several years of buoyant rural conditions. However, we expect tailwinds will become headwinds as livestock and other commodity prices retreat to more normal levels over the next two years. We hold an underweight rating.

Elmo Software (ELO)

This cloud-based solutions provider has steadily increased revenue in recent years. But costs have also been rising. The company expects it will become cash flow positive in the second half of fiscal year 2023. In today’s market, we believe there are more attractive, lower risk alternatives, so we retain an underweight rating.

Braden Gardiner, Tradethestructure.com

BUY RECOMMENDATIONS

Iress (IRE)

First half fiscal year 2022 segment profit is expected to be $80.3 million, up 6 per cent on the prior corresponding period, according to unaudited results. Shares in this software provider to the financial services sector have risen from $9.75 on June 15 to trade at $11.42 on July 28. From a technical perspective, I expect to see a move up to $15 if the stock can continue holding higher levels.

Orica (ORI)

Since the lows in September 2021, this explosives producer has been moving steadily higher, even taking market weakness in its stride. I expect momentum to push the price through pre-pandemic highs of around $18 if it stays above the closing price of $15.05 on June 20.

HOLD RECOMMENDATIONS

Silex Systems (SLX)

A non-binding letter of intent has been executed between Global Laser Enrichment (GLE) and Constellation Energy Generation to assess areas of co-operation in the nuclear fuel supply chain. GLE is the exclusive licensee of Silex laser technology. SLX shares responded positively to the announcement. The shares were priced at $1.28 on May 25. The stock was trading at $3.39 on July 28.

West African Resources (WAF)

With spot gold prices recently falling, WAF has done well to hold around recent highs and above $1.15 a share. The share price has risen steadily from lows around 40 cents in March 2020. WAF is worth holding above $1.15 to see if any gold price recovery sends the shares higher. The stock was trading at $1.315 on July 28.

SELL RECOMMENDATIONS

Mineral Resources (MIN)

This mining services company focuses on the iron ore and lithium sectors in Western Australia. The share price has fallen from $63.85 on May 31 to trade at $52.36 on July 28. Any falls in iron ore and lithium prices are likely to weigh on MIN, in our view. It may be time to take some risk off the table.

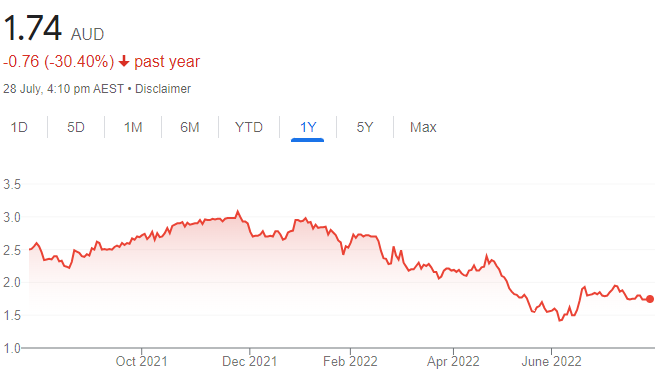

Corporate Travel Management (CTD)

The CTD share price has fallen from $26.25 on April 29 to trade at $19.16 on July 28. Any move below $17.40 may trigger more investors to exit the stock. The company is exposed to a volatile global travel sector in challenging pandemic and economic times. Other stocks appeal more at this stage of the cycle.

The above recommendations are general advice and don’t take into account any individual’s objectives, financial situation or needs. Investors are advised to seek their own professional advice before investing. Please note that TheBull.com.au simply publishes broker recommendations on this page. The publication of these recommendations does not in any way constitute a recommendation on the part of TheBull.com.au. You should seek professional advice before making any investment decisions.